Employees are required to make advance payments toward their income tax. This so-called payroll tax is automatically deducted from their paychecks. The amount of payroll tax you owe depends on your tax bracket. There are seven different tax brackets to distinguish between. As tax advisors in Düsseldorf

and Oberhausen

, we see every day that many taxpayers do not know which tax brackets exist or how their own tax bracket is structured. To clarify what each tax bracket means and which bracket you are assigned to, we explain this in this article.

General Information on Tax Brackets

Employees are assigned a tax bracket by the tax office. Income tax is calculated based on this tax bracket. Entrepreneurs and self-employed individuals, on the other hand, do not have a tax bracket because they do not pay income tax. Entrepreneurs must make individual income tax prepayments. Which of the seven tax brackets an employee falls into depends primarily on their marital status. In some cases, a change of tax bracket can be requested. In most cases, however, it is automatically assigned by the tax office. It is important to note that tax classes only become relevant once monthly earnings exceed €450. The deductions are similar across all tax classes. Employees must accept the following deductions:

- Long-term care insurance

- Health insurance

- Unemployment insurance

- Pension insurance

- Income tax

- Church tax

- Solidarity surcharge

The deductions and taxes listed are calculated as a percentage of income. There are differences between tax brackets, particularly regarding allowances and flat rates. As a result, you will face more or fewer deductions depending on your tax bracket. The following sections explain all tax brackets in detail.

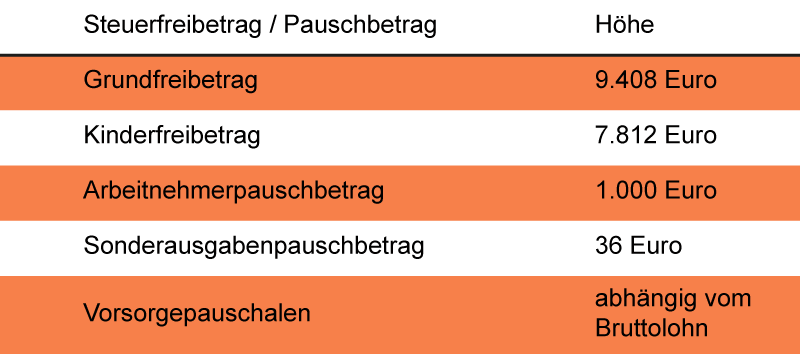

Tax Class 1 – Income Tax for Singles

Tax class 1 can be described as the standard tax class. All employees who are single, widowed, divorced, or permanently separated fall into tax class 1. Most taxpayers will start their working lives in this tax class. Only after your family situation changes or you have children does the tax class adjust to your new circumstances. The following tax allowances and flat-rate amounts currently apply in income tax class 1:

Generally speaking, your tax burden is higher in tax class 1 than in other tax classes. Taxpayers with children or a spouse can benefit from additional tax relief. Similarly, the higher gross salary taken into account is also an advantage because you also receive higher wage replacement payments. If unemployment benefits, sick pay, or parental leave benefits are claimed, taxpayers in tax class 1 often receive slightly higher payments. However, as a taxpayer in tax bracket 1, there is no need to consider the pros and cons any further. A switch to another tax bracket is only possible anyway if your family situation changes. Until then, employees are tied to tax bracket 1.

Generally speaking, your tax burden is higher in tax class 1 than in other tax classes. Taxpayers with children or a spouse can benefit from additional tax relief. Similarly, the higher gross salary taken into account is also an advantage because you also receive higher wage replacement payments. If unemployment benefits, sick pay, or parental leave benefits are claimed, taxpayers in tax class 1 often receive slightly higher payments. However, as a taxpayer in tax bracket 1, there is no need to consider the pros and cons any further. A switch to another tax bracket is only possible anyway if your family situation changes. Until then, employees are tied to tax bracket 1.

Tax Class 2 – Tax Benefits for Single Parents

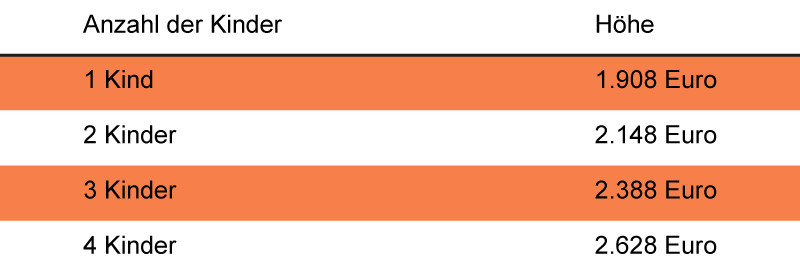

The tax office has established a special tax bracket for single parents. The financial burden in these families is often particularly high. Taxpayers who must raise a child on their own should therefore receive tax benefits. The tax benefit is provided through an additional tax relief amount. This amount is granted in addition to child benefit and the child allowance. To take advantage of the relief amount, single parents are not required to be in tax class 2. The relief amount can also be claimed on the tax return at the end of the year. You will then receive a refund. However, it makes much more sense for single parents to switch to tax class 2 and thereby reduce their monthly income tax withholding. Tax allowances and flat-rate amounts correspond to those in tax class 1. In addition, the relief amount is as follows:

To apply for the change in tax bracket and gain access to the aforementioned tax brackets, certain requirements must be met. The exact definition can be found in the Income Tax Act under §24b. The following requirements must be met:

To apply for the change in tax bracket and gain access to the aforementioned tax brackets, certain requirements must be met. The exact definition can be found in the Income Tax Act under §24b. The following requirements must be met:

- You are an employee subject to social security contributions

- You live with your child in a shared residence where the child is also registered

- You are eligible for child benefit and/or the child tax credit

- You are not married and do not share a household with another adult

In some cases, children are registered with both parents. In such cases, the tax relief amount is paid to the person who receives the child benefit. If all the above conditions are met, you may apply to switch to tax class 2. If you wish to benefit from these advantages, do not forget to submit the appropriate application. The switch does not occur automatically!

Tax Class 3 – Spouse in combination with Tax Class 5

Tax class 3 can only be chosen by married taxpayers. This tax class becomes relevant when one spouse earns significantly more money than the other. Switching to tax class 3 allows the spouse with the higher income to pay less tax. By making this switch, spouses choose to file their taxes jointly. The other spouse must switch to tax class 5. The government primarily intends this tax class to benefit families. However, this option only makes sense if one spouse earns less. It becomes worthwhile if one person contributes more than 60% of the total income. Otherwise, tax class 4 may be more attractive.

If the combination of tax classes 3 and 5 is selected, the income is assessed jointly. All allowances from both partners are applied to the higher income. The higher deductions thus apply to the spouse with the lower income. In many cases, this results in a higher total income over the course of the year. Whether this tax bracket is worthwhile for you should be discussed with a tax advisor.

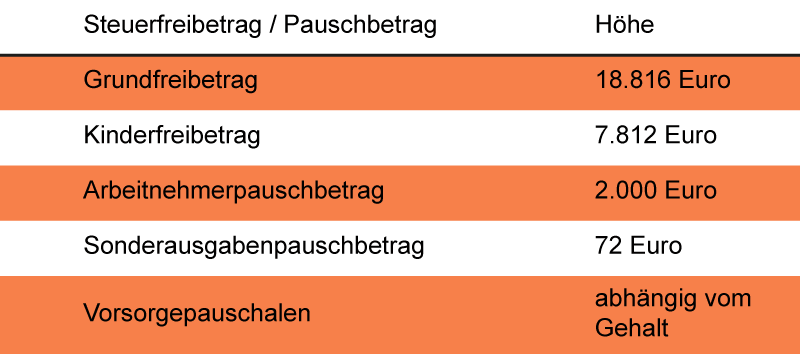

The deductions do not change in tax bracket 3. The higher allowances and flat-rate amounts are of interest. In 2020, the following amounts apply in tax bracket 3:

Tax Class 4 – Benefits for Spouses with Equal Incomes

Tax class 4 is also intended for spouses. Taxpayers who are newly married are automatically assigned to tax class 4. The deductions do not differ from those in other tax classes. However, the tax burden is comparatively high. The tax bracket therefore only makes sense in specific income structures. An alternative could be a combination of tax brackets 3 and 5 or switching to tax bracket 4 with a factor. Tax allowances and flat-rate allowances correspond to tax bracket 1.

Tax Class 4 with a factor – Spouses with differing incomes

Spouses who earn similar amounts can simply remain in tax class 4. As soon as you and your spouse have different income levels, switching to tax class 4 with a factor may make more sense. For this special tax bracket, an individual factor is determined. The estimated annual income is used as a guide. Using the splitting method, the estimated income tax is calculated based on this factor. The advantage: The couple can benefit from the splitting advantage already during the year. Additionally, back taxes are avoided. However, compared to the combination of tax classes 3 and 5, you will generally end up paying slightly more in taxes. It’s also important to note that filing a tax return is mandatory in tax class 4 with a factor.

Tax Class 5 – The Counterpart to Tax Class 3

Tax class 5 is only relevant in combination with the previously explained tax class 3. If one spouse moves to the more favorable tax class 3, the other must automatically move to tax class 5. The combination of tax classes 3 and 5 is only worthwhile if the spouse in tax class 3 earns significantly more. The spouse in tax bracket 5 should therefore earn as little as possible. The lower income is taxed at a higher rate in tax bracket 5. There is no annual tax-free allowance in tax bracket 5; this is effectively transferred to the other spouse. In addition, filing a tax return is mandatory. Due to the large difference in income, this combination can still result in very significant tax savings during the year. The extent to which you can benefit should be discussed individually with a tax advisor.

Tax Class 6 – Employees with Second and Part-Time Jobs

Some employees have additional jobs in addition to their primary employment. Tax class 6 applies if you have a second or side job and it exceeds the 450-euro threshold. In addition to the standard tax class, a second one is then required for the side job. This second tax bracket is always Tax Bracket 6. This tax bracket is very unpopular because it carries the highest tax rates compared to all other brackets. For Tax Bracket 6, all tax-free allowances are eliminated. Tax deductions are therefore not reduced and remain comparatively high. As tax advisors, we therefore always advise our clients to first assess whether the side job is worth it after deductions. In some cases, for example, it may be more attractive to take on a mini-job rather than a side job with a higher salary and higher deductions.

Any questions? Tax consulting in Düsseldorf and Oberhausen

We hope you now have a better understanding of how tax brackets work. You may even know more about your own tax bracket or have identified the potential for a more attractive change. If you still have questions regarding tax brackets or, as a business owner, would like to learn more about calculating advance payments, we are the ideal point of contact. Our team of qualified tax advisors answers tax questions and assists you with your tax return. Contact us to schedule a consultation.