Employers are increasingly demanding greater mobility from their employees. However, many employees do not want to burden their families with a move and therefore commute daily between their home and workplace. For commuters, this means long daily commutes and high fuel costs. The solution is increasingly to establish a second household in addition to the primary one. This results in “maintaining two households.” If employees opt for a second residence, this is often supported by the tax authorities.

Under certain conditions, employees can claim expenses related to maintaining two households as income-related expenses on their tax returns. For business owners or self-employed individuals, these expenses may qualify as business expenses against income from business operations or self-employment.

If the tax office recognizes the dual household arrangement, filing an income tax return reduces one’s tax burden. The following discusses the dual household arrangement from the employee’s perspective. However, the conditions outlined also apply to business owners and self-employed individuals.

When does maintaining two households apply?

From a tax perspective, the following requirements must be met for a dual household arrangement to apply. If this is not the case, the expenses cannot be included in the tax return.

- Separate household at the primary residence

A “primary residence” with a separate household must be maintained at the actual place of residence. The residence must be owned by the employee or rented by them. The residence must be furnished to meet the employee’s living needs. The center of the employee’s life interests must be permanently located at the primary residence. Financial contribution to household expenses is also a requirement. According to the tax office, “trivial amounts” are not sufficient. A financial contribution of more than 10% of the monthly household expenses is considered the minimum. If the center of life’s interests shifts from one’s own household to the place of employment, the professional justification ceases to apply, and thus the maintenance of two households.

A “primary residence” with a separate household must be maintained at the actual place of residence. The residence must be owned by the employee or rented by them. The residence must be furnished to meet the employee’s living needs. The center of the employee’s life interests must be permanently located at the primary residence. Financial contribution to household expenses is also a requirement. According to the tax office, “trivial amounts” are not sufficient. A financial contribution of more than 10% of the monthly household expenses is considered the minimum. If the center of life’s interests shifts from one’s own household to the place of employment, the professional justification ceases to apply, and thus the maintenance of two households.

- Place of employment outside the local area

In addition to the primary residence, a second residence must be maintained at the place of employment. The distance between the primary residence and the residence at the place of employment is generally irrelevant. In cases of very short commutes, the tax office may not recognize the dual household arrangement. However, there are no specific guidelines from the tax office on this matter. It is therefore always necessary to consider each case individually. For the sake of simplicity, a dual household arrangement can be assumed if the distance from the secondary residence to the workplace is less than half the distance of the shortest route between the primary residence and the place of work.

Example: The employee has his household in Düsseldorf and his workplace in Frankfurt am Main. The distance from Düsseldorf (center of life interests) to Frankfurt is approximately 250 km. The employee immediately finds an affordable second residence in Koblenz. The distance from Koblenz (second residence) to Frankfurt is 120 km. Even though the second residence is 70 km from Frankfurt, it is still considered a residence at the place of work because it is less than half the distance from the primary residence in Düsseldorf to the workplace in Frankfurt.

In practice, however, there are frequent deviations from this rule. Therefore, you should always consult with a tax advisor beforehand.

- Work-related reason

The second residence must be used regularly for professional reasons. If the professional necessity no longer applies, the second residence is no longer considered a dual household. Consequently, the costs can no longer be deducted.

Which costs can be deducted?

If the aforementioned requirements for maintaining two households are met, many costs can be claimed for tax purposes. Below, we provide an overview of which expenses can be claimed:

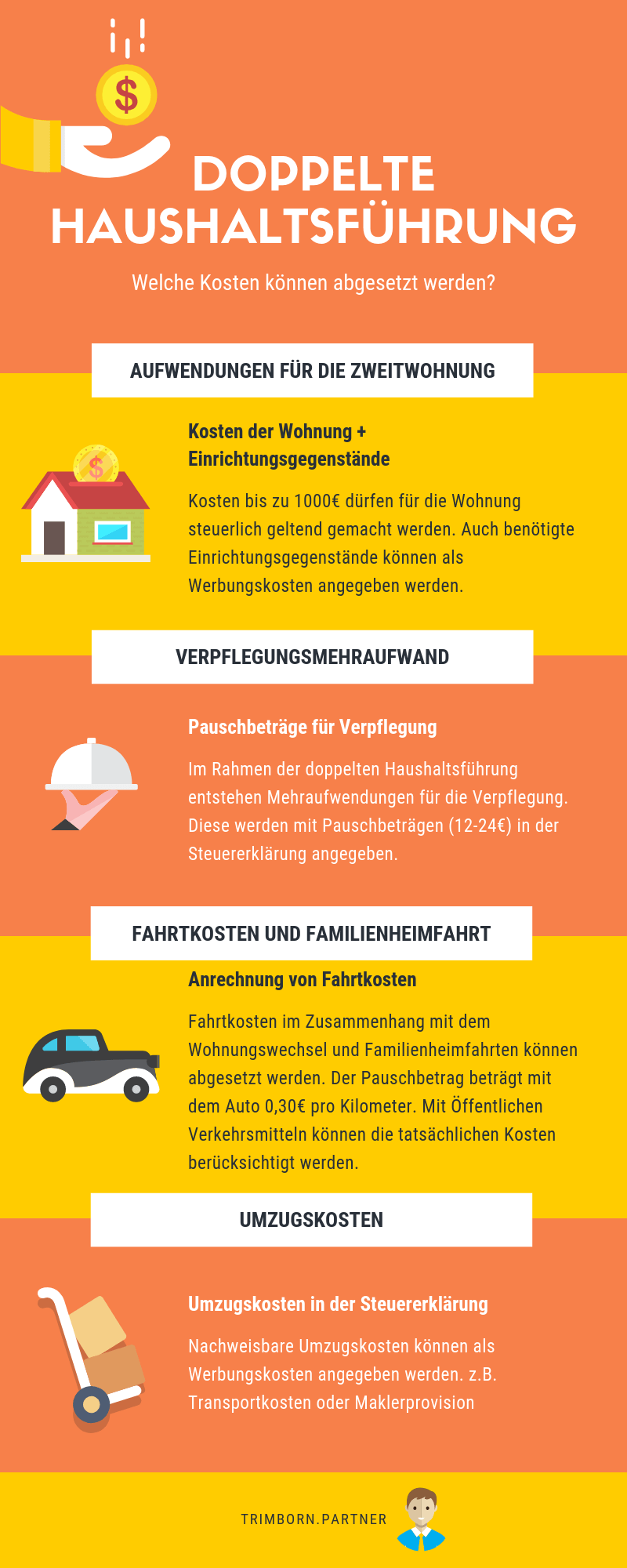

- Expenses for the second residence

A second home is defined as any accommodation made available to the employee, whether for a fee or free of charge. You can therefore choose between:

- a rented apartment

- a furnished room

- a hotel room

- a guesthouse

- shared housing

- a condominium

The employee may claim all actual expenses for one of the aforementioned types of housing in cases of maintaining two households, up to a maximum of €1,000 per month.

For a rented apartment, the deductible expenses include:

- Base rent

- Utilities (electricity, heating, garbage collection, etc.)

- Wages for a domestic helper

- Renovation expenses

If the employer decides instead to purchase a condominium, they can claim the costs in the same amount as they would for a rental apartment. The maximum amount is also €1,000 per month.

Costs for the furnishings needed in the second home can also be claimed. These include:

- Bed, wardrobe, table, chairs, sofa, curtains, lamps, stove, sink, refrigerator, and washing machine

- Household items such as dishes, pots, coffee maker, and vacuum cleaner

Caution is advised regarding “unreasonably” high costs. Expensive built-in kitchens or similar items are often not recognized by the tax office.

- Additional meal expenses

In the context of maintaining two households, the employer incurs additional meal expenses that would not arise if meals were provided in only one household. These additional expenses can be claimed for tax purposes. However, only flat-rate amounts are taken into account. Additional meal expenses are recognized for a period of three months after moving into the second residence at the place of work, for each calendar day on which the employee is absent from the residence at the shared primary residence. The amount of the lump-sum amounts of €12 or €24 is determined by the duration of the absence.

- Travel expenses and trips home to the family

Travel expenses related to the move at the beginning and end of the dual-residence period may be claimed in the actual and documented amount (e.g., train ticket). Alternatively, they may be claimed in the amount of the flat rates (€0.30 per kilometer driven for car travel) for business travel.

Travel costs from the place of employment to the employee’s own household and back may also be deducted. However, only one trip home per week is allowed. If a car is used, €0.30 per kilometer traveled may be claimed. A trip home using public transportation may be claimed at the actual cost.

- Moving expenses

Verifiable moving expenses can also be claimed as income-related expenses.

Relocation costs include:

- Costs of finding housing (e.g., real estate agent’s commission)

- Transportation costs (e.g., moving company or truck rental)

- Tips for moving personnel

- Connection fees for the stove, etc.

Any questions? Consult a tax advisor!

The topic of maintaining two households often raises unanswered questions. We hope this article has addressed some of the most important ones. Do you have further questions, or are you considering setting up two households yourself? As tax advisors in Düsseldorf and Oberhausen, we look forward to providing you with a detailed consultation. Contact us to schedule an appointment.